.png)

What is the creator economy? It’s defined as the class of businesses built by over 50 million independent content creators, curators, and community builders including social media influencers, bloggers, and videographers, plus the software and finance tools designed to help them with growth and monetization.

The three top trends in the creator economy are:

- Creators moving their top fans off of social networks and on to their own websites, apps, and monetization tools

- Creators becoming founders, building out teams and assembling tools to help them start businesses while focuses on their art

- Creators gaining power in the media ecosystem as fans seek to connect with individual personalities rather than faceless publishers

More than 50 million people around the world consider themselves creators, despite the creator economy only being born a decade ago. It’s become the fastest-growing type of small business, and a survey found that more American kids want to be a YouTube star (29%) than an astronaut (11%) when they grow up.

Subscribe to SignalFire’s newsletter for guides to startup trends, fundraising, and recruiting.

We’ve created a crash course on over 100 of the top startups and tools built to help influencers, so whether you’re a creator seeking help, a founder identifying opportunities, or an investor looking for the next rocketship, this market map will give you both a broad and deep view of the creator ecosystem. I promise that the next 10 minutes of your reading will not be interrupted by ads. No premium membership required.

Using platforms like YouTube, Instagram, Snapchat, Twitch, TikTok, Substack, Patreon, and OnlyFans, content creators can earn money through:

- Advertising revenue shares

- Sponsored content

- Product placement

- Tipping

- Paid subscriptions

- Digital content sales

- Merchandise

- Shout-outs

- Live and virtual events

- VIP meetups

- Fan clubs

If you are a founder building something special in this space, SignalFire would love to hear from you! We’ve funded tools to help influencers operate and monetize like credit card Karat, and led the seed round for YouTube co-founder Chad Hurley’s new company GreenPark. We fund both early and mid-stage startups, and help them with recruiting, advising, go-to-market strategies, and PR. So don’t be shy about sliding into our DMs or smashing this newsletter subscribe button.

So how did creatorship grow so quickly? There’s been a societal shift in consciousness towards caring more about feeling fulfilled in our jobs, having control over how we spend our time, and being our own boss. Fans see creators doing what they love for a living and aspire to follow that path that never leads to a cubicle.

Meanwhile, better cameras on phones, larger screens, faster mobile networks, and creator-focused social networks have spurred an inflection point for the industry. Now all you need to join the creator club is a phone, an idea, and a willingness to be judged by strangers. Simple? Not quite. That will guarantee you 12 views (maybe 15 if you have many cousins). And don’t even dream about brand deals. To succeed, creators have to be incredible storytellers, relentless hustlers, and leaders of their fan communities.

Luckily, a ton of companies have been built to support creators, especially the 2 million people able to make a full-time career out of it (just imagine all the tools and infrastructure that are needed if the entire population of Lithuania were to become YouTubers).

Subscribe to SignalFire’s newsletter for guides to startup trends, fundraising, and recruiting.

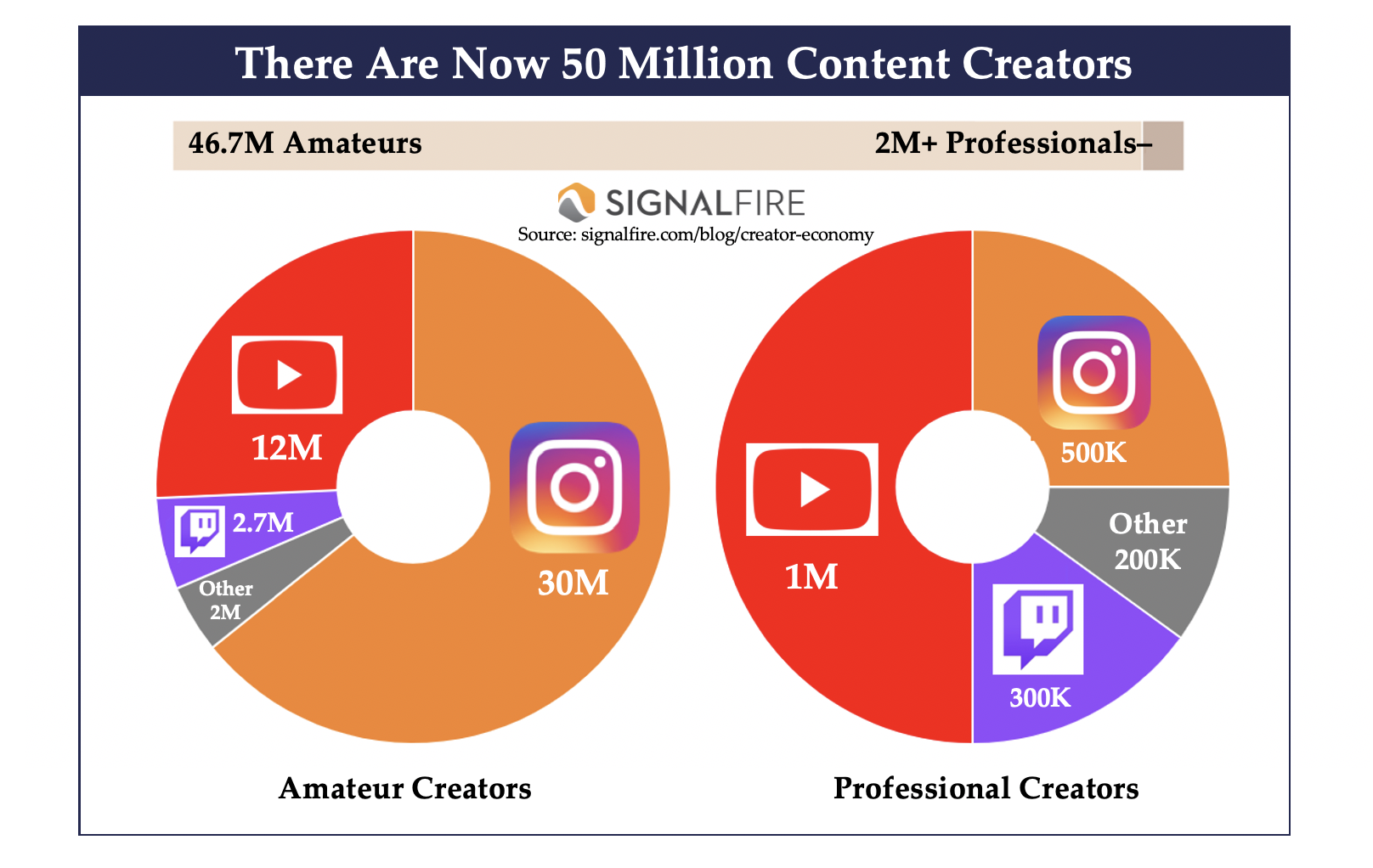

How many creators are there?

Here’s our bottom’s up TAM (total addressable market) analysis, which adds up to 50 million creators:

- Professional Individual Creators (~2M+) – Making content full-time

- YouTube: Of the 31M channels on YouTube, ~1M creators have over 10K subscribers (source)

- Instagram: Of the 1bn accounts on Instagram, ~500K have over 100k followers and are considered active influencers (source)

- Twitch: Of the 3M streamers on Twitch, ~300K have either Partner or Affiliate status (source)

- Others: including musicians, podcasters, writers, illustrators, etc total ~200K

- Amateur Individual Creators (~46.7M) – Monetizing content creation part-time

- YouTube: Of the 31M channels on YouTube, ~12M have between 100-10K subscribers (source)

- Instagram: Of the 1bn accounts on Instagram, ~30M have between 50-100K followers (source)

- Twitch: Of the 3M streamers on Twitch, ~2.7M are non Partner or Affiliates

- Others: including musicians, podcasters, writers, illustrators, maybe a total of ~2M

Here’s a video from SignalFire’s Wayne Hu that reveals how the creator business grew so fast:

State Of The Creator Economy: A Brief History

Before we dive into all the types of tools, it’s important to understand the evolution of the creator economy, which can be divided into 3 distinct layers that build on each other.

- Layer 1: Foundational Media Platforms. Since the late 2000s, we witnessed the birth of platforms like YouTube, Instagram, iTunes, Spotify, and more recently Snapchat, Twitter, Medium, Twitch, TikTok, etc. Platforms help creators get discovered and establish an audience by investing heavily in their recommendation and curation algorithms — they solved the distribution problem for creators. No longer were creators at the mercy of large production companies who decided what content to produce and who the audience would be. These platforms contributed to the rise of multi-channel networks like Maker and Fullscreen. They aggregated creators and equipped them with audience development tools before they were bought for hundreds of millions, while new networks like Brat TV and Tastemade emerged. The platforms also necessitated the creation of multimedia editing tools that helped creators polish their content. But platforms don’t always have content contributors’ best interests in mind so the smart creators learn to cross-promote and diversify their presence on different apps to minimize “platform risk”. That way they’re not vulnerable to one platform’s decline, change in priorities, removal of features, or reduction in opportunities that can hurt them, which is known as “platform whiplash”.

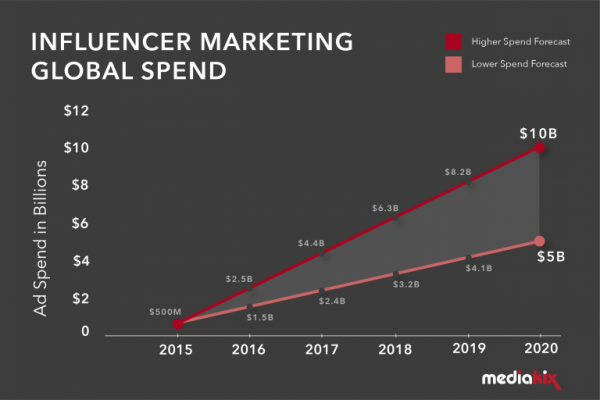

- Layer 2: Monetizing Influencer Reach. Once top creators had built an established audience who trusted what they had to say, brands started to recognize the return on investment of paying creators to harness their on-platform reach to advertise products and services. While some platforms split traditional ad revenue with creators, others left it up to the content makers to figure out how to monetize, leading to the rise of sponsored content and companies like Niche that brokered the deals. There are now hundreds of companies in this space including influencer agencies, sponsorship marketplaces, talent representation companies, and more. According to Mediakix, the current influencer marketing TAM is ~$8bn and it’s expected to grow to $15bn by 2022, making it one of the fastest-growing business sectors. Ideally, creators work with sponsors that match their personal brand, and don’t sacrifice content quality to overtly push a corporate message. However, as influencer marketing grew more common and more brands started paying for it, influencers noticed a pattern: with each paid post, they’d lose some of the trust that they established with their audience, hurting their engagement and growth. Which brings us to the latest wave of creators’ evolution…

- Layer 3: Creators as businesses. This is where we are today! Having developed fandoms that follow them off-platform, creators can become full-fledged businesses with multiple revenue streams beyond ads. Companies have arrived to help creators earn money by selling products such as premium content, merchandise, books/ebooks, newsletters, or selling services such as fan engagement, coaching, consulting, speaking engagements, etc. This lets creators focus on delighting their biggest fans and making more unique niche content, rather than desperately seeking the biggest possible audience and making more generic clickbaity content.

Essentially, creators have to balance the distribution potential of certain platforms with the risk of becoming dependent on them, and monetize by either earning a little off of each fan from mainstream content for a big audience or earning a lot off of deeper connections to a smaller set of fans through niche content.

The big trend we see here is that over time, creators are becoming more diversified in their revenue streams and are being funded directly by their fans.

Creators have shifted from being paid by platforms like YouTube with ad revenue shares in exchange for bringing in an audience to the platforms, to being paid by brand sponsors on Instagram and Snapchat in exchange for their reach to an audience they access through the platforms, to being paid by fans via patronage or tipping or ecommerce in exchange for entertainment and community beyond the platforms.

Now that we’ve gotten the brief history lesson out of the way, let’s talk about specific subsectors and exciting companies within them! We’ll also discuss the COVID-19 impacts as well as our assessment of the investment opportunities within each.

Layer 1: Birth of Media Platforms

Media Platforms

A list of all the usual suspects. No additional explanation needed, right?

- Video / Streaming: YouTube, TikTok, Twitch, Instagram Live, Facebook Live, YouNow, Vine, OnlyFans

- Photography / Graphic Design: Instagram, Snapchat, Pinterest, VSCO

- Music / Podcast: iTunes, Spotify, Pandora, Soundcloud

- Writing: Twitter, Medium, Quora, Substack

COVID-19 Impact? Large tailwinds as consumer engagement in entertainment has increased. As users spend more time on these apps, they follow more creators, consume more of their content, and earn them more money. This, in turn, can grow the platforms’ revenues while making creators more willing to pay for tools that help them.

Opportunity Assessment

- Pros: Once these platforms gain traction they can grow rapidly thanks to virality. There have been huge outcomes in this space.

- Cons: Very saturated market with the winners in each category already identified. Difficult for new entrants as incumbents all have strong network effects.

Content Creation Tools — Without Networks

Some platforms have their own embedded content creation tools (i.e. TikTok video effects and Instagram photo filters) but there are many companies that provide point solutions for making enhanced content. Historically, content creation tools with social networks attached have been the most financially successful.

One meaningful exception is the giant incumbent in this space, Adobe Creative Cloud, which includes Photoshop and several other famous tools like Premier Pro and Illustrator. In 2013, Adobe shifted its business model from selling individual software licenses ($1,300-$2,600 for the full suite) to selling a subscription ($52/month for the full suite). However, the majority of Adobe’s customers are business creators (i.e. people who work on the marketing team of some corporation) as opposed to the individual creators who publish on the social platforms.

Some platforms have made acquisitions to become an “all-in-one” destination for discovery, creation, and monetization. In 2017 Spotify acquired Soundtrap, a music production software developer, so it could offer ways to make music rather than just distribute it.

Today, it’s common for creators to cobble together multiple tools for editing and earning money off their content they then share on social networks. For example, Instagram creators might finance a shoot with Karat, record in Snapchat, edit with inVideo or Pixlr, then post to Instagram where they monetize on platform with Grin or Captiv8, earn money off-platform with Teespring and Cameo, and track their analytics with Delmondo.

A breakdown of content creation tools by type of media:

- Video: Streamlabs’ OBS (Open Broadcaster Software), an open-source app for recording livestreamed video, Tools like inVideo and PlayPlay are mobile and web-based video editing tools that help creators format their videos into socially shareable formats on Instagram, Facebook, etc. Vochi is an app-based video editor that takes it a step further and makes really cool video effects. Other tools like Kapwing take a more horizontal approach and help with editing video, audio, and even GIFs. Apps like Trash and Quik automatically edit together short video clips with music to make mini-movies you can share in Trash or on any social network. Creators are even renting out rooms by the hour on PeerSpace and Breather so they have a place to shoot their videos.

- Photography / Graphic Design: Affinity is a UK-based company that has been challenging Adobe’s throne. At only $50 per full access license, Affinity offers a much more affordable professional photo, design, and layout editor for creators. Other low-cost web-based photo editors include Pixlr, PicMonkey, and Fotor. Companies like Canva and Snappa focus more on being a graphic design editor for all mediums — flyers, business cards, brochures, invitations, photos, etc. Then there are also companies like Piktochart that are made for infographic design. And of course, Meitu and FaceTune let users smooth out blemishes, whiten their teeth, and even change the shape of their face to appear more attractive. Canva has recently been making headlines with its $6 billion valuation, making it arguably one of the most valuable content creation companies in recent years. Surprisingly, all of Canva’s revenue comes from individuals upgrading to a premium membership, which gives users instant access to 60K templates (vs. only 8K for the free tier) and a library of 60 million stock photos, GIFs, videos, graphics, etc. What makes Canva a 10X better tool than all the others is their extensive treasure chest of design building blocks that make it easy to create something beautiful.

- Motion Photos: Apart from the two largest GIF creation platforms Giphy and Gfycat, a new type of media format, the “video meme”, has been on the rise. Check out Pinata, which should be launching its public beta soon.

- Music: There are really not that many startups in this space, probably because it’s a much smaller market than some of the other media formats. Many artists use GarageBand which has most of the basic functionalities to create music. Professionals might purchase a license from one of the several large, legacy companies that sell downloadable music production software such as FL Studio and Ableton Live, or turn to Splice for music production collaboration and either buying or selling audio samples for use in songs. Meanwhile, distribution through streaming platforms, marketing via social networks, monetization through patronage platforms, the death of physical formats like CDs have eliminated many of the needs for traditional record labels.

- Podcast: A hot space as the podcasting format has become more popular in recent years. One of SignalFire’s portfolio companies, RedCircle, helps podcasters reach new audiences and monetize their content by connecting them with brands for advertising opportunities. Other companies that help with publishing podcasts include PodBean, Megaphone, Buzzsprout, and Anchor.

COVID Impact? Large tailwinds as more people are staying at home and either becoming creators for additional sources of income or existing creators have more time to devote to their creations.

Investment Opportunity Assessment

- Pros: Innovative tools that get adopted by creators can go viral on social media.

- Cons: Adobe is a huge incumbent in this space with clear network effects (it has become such a standard of file types that enables sharing amongst creators). Point solutions for creators are tough to monetize unless it has a clear ROI for the creator / product is very differentiated and defensible.

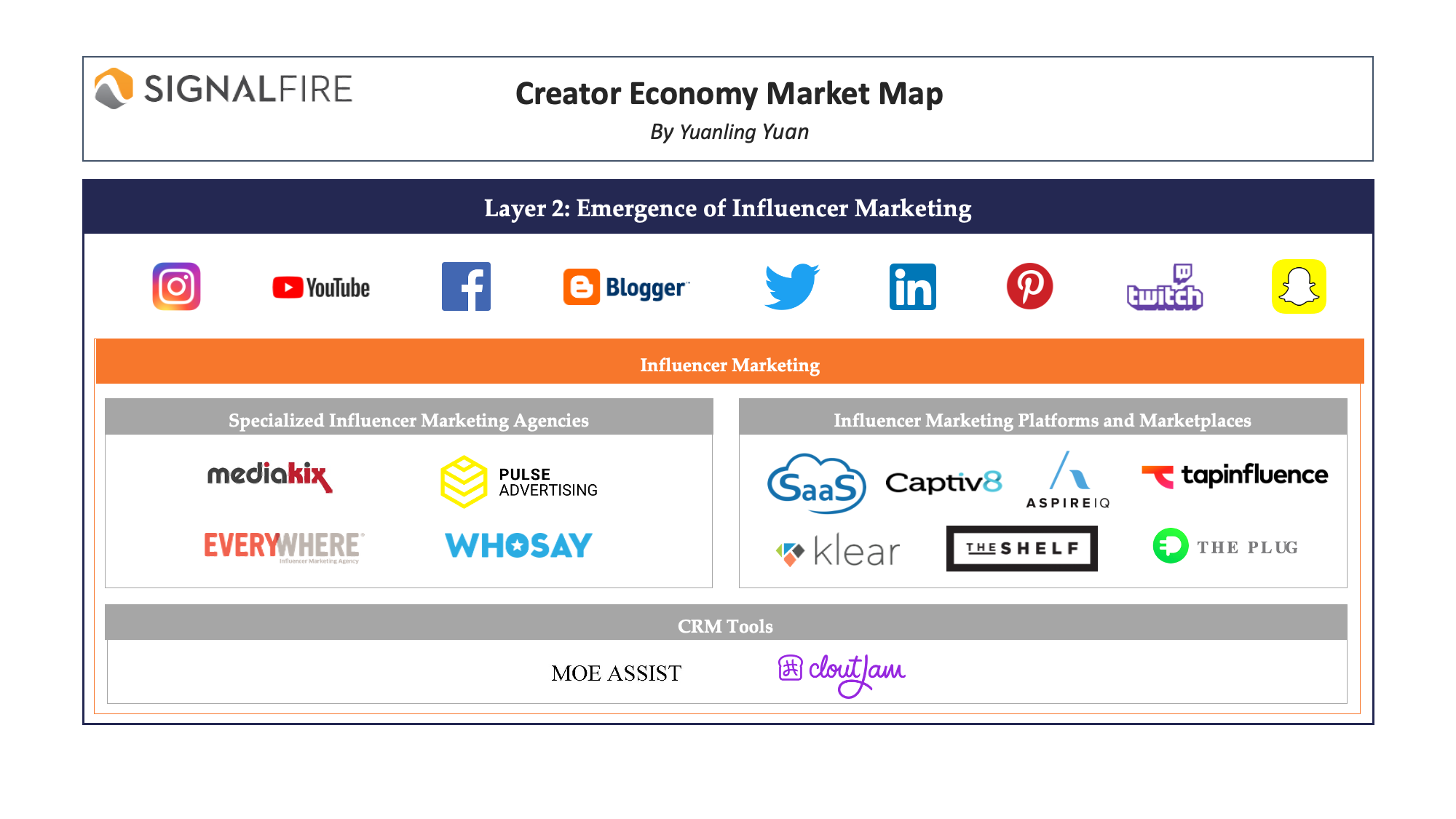

Layer 2: Emergence of Influencer Marketing

Influencer Marketing

There are several types of companies in this space:

- Specialized Influencer Marketing Agencies. Brands hire these agencies to identify high-performing influencers to reach specific audience demographics, negotiate influencer contracts, maintain consistent communication with influencers, launch multiple cross-channel campaigns, and conduct in-depth post-campaign analysis as well as ROI assessments. The largest dedicated influencer agencies include Mediakix, Pulse Advertising, WHOSAY, and Everywhere. Brands hire them because they don’t have direct connections to influencer talent or in-house teams to work with them. But because these agencies are extremely hands-on and personalized, they are very expensive for both the brands and influencers. PR giants like Edelman and Weber Shandwick have also joined in as middlemen between creators and brands while ensuring their clients aren’t besmirched.

- Influencer Marketing Platforms and Marketplaces. For brands, this is a much cheaper solution to access a large database of influencers that they can filter from. The platforms typically charge a Software-As-A-Service fee plus a take rate on each campaign. While the platforms may have built-in analytics and reporting capabilities, the downside is that brands typically won’t get access to the largest influencers as those usually only work with agencies. The supply is mostly on small-to-medium-sized influencers that may not have as wide of a reach and thus, ROI on marketing spend. Some influencer marketing platforms include Grin, Captiv8, AspireIQ, Tapinfluence, Klear, The Shelf, CreatorIQ, and Arthouse (formerly Niche, owned by Twitter) where brands are able to set a budget for their campaigns and search the large database of influencers who meet their criteria. Traditional Hollywood talent agencies like CAA, UTA, and WME often partner with the influencer marketing giants to make their mainstream celebrities available to brands. Platforms like The Plug take a different approach by giving influencers the power to choose which campaigns they want to work with. However, advertisers on their platform only pay on a performance basis (i.e. if someone downloads the advertiser’s app). Unlike traditional brand campaigns, the influencer’s pay, in this case, is directly proportional to the ROI they generate for the brand. Platforms like Pixlee help brands automatically find and curate content created by their users on social media, which can sometimes be more cost-effective and authentic because viewers know that the content was generated by an existing customer. Other players in this more quantified influencer marketing and analytics space include: Collectively and theAmplify (owned by You & Mr Jones), Delmondo (owned by Conviva), and Whalar. Fans and brands alike look to the rankings on Famous Birthdays, the Wikipedia of influencers, to find stars to follow or work with. Some influencers sell creative services for conceptualizing and producing content without having to spam their followers, some focus on the low-effort business of selling distribution of existing content to their huge audience, and some do both.

.png)

- CRM Tools. Since influencers sign up for multiple influencer marketing platforms and often have several brand contracts going on simultaneously, CRM tools built specifically for influencers like Tubular Labs, MoeAssist, and CloutJam have recently popped up to help influencers manage their workflow.

COVID Impact? Minor tailwinds as corporate and brands cannot do in-person professional shoots so they are reaching out to creators for user-generated content, but other brands have largely paused marketing efforts to conserve cash.

Investment Opportunity Assessment

- Pros: There is an opportunity to build a large, scalable business in the platform/marketplace segment given that brand marketing is still the #1 way that creators generate income. Who will be the DoubleClick of influencer marketing

- Cons: There has been no major outcome in this space, with Twitter’s buy of Niche and Google’s acquisition of FameBit only ranging in the tens of millions. Our hypothesis is that there are several reasons why:

- None of these platforms can monopolize on supply — influencers are incentivized to sign up with as many of them as possible. Defensibility is a key question.

- Top influencers work with agencies, not platforms/marketplaces. These platforms typically capture a long tail of small to medium-sized influencers.

- Influencers all have distinct personalities and are thus hard to manage — platforms are not equipped to do so.

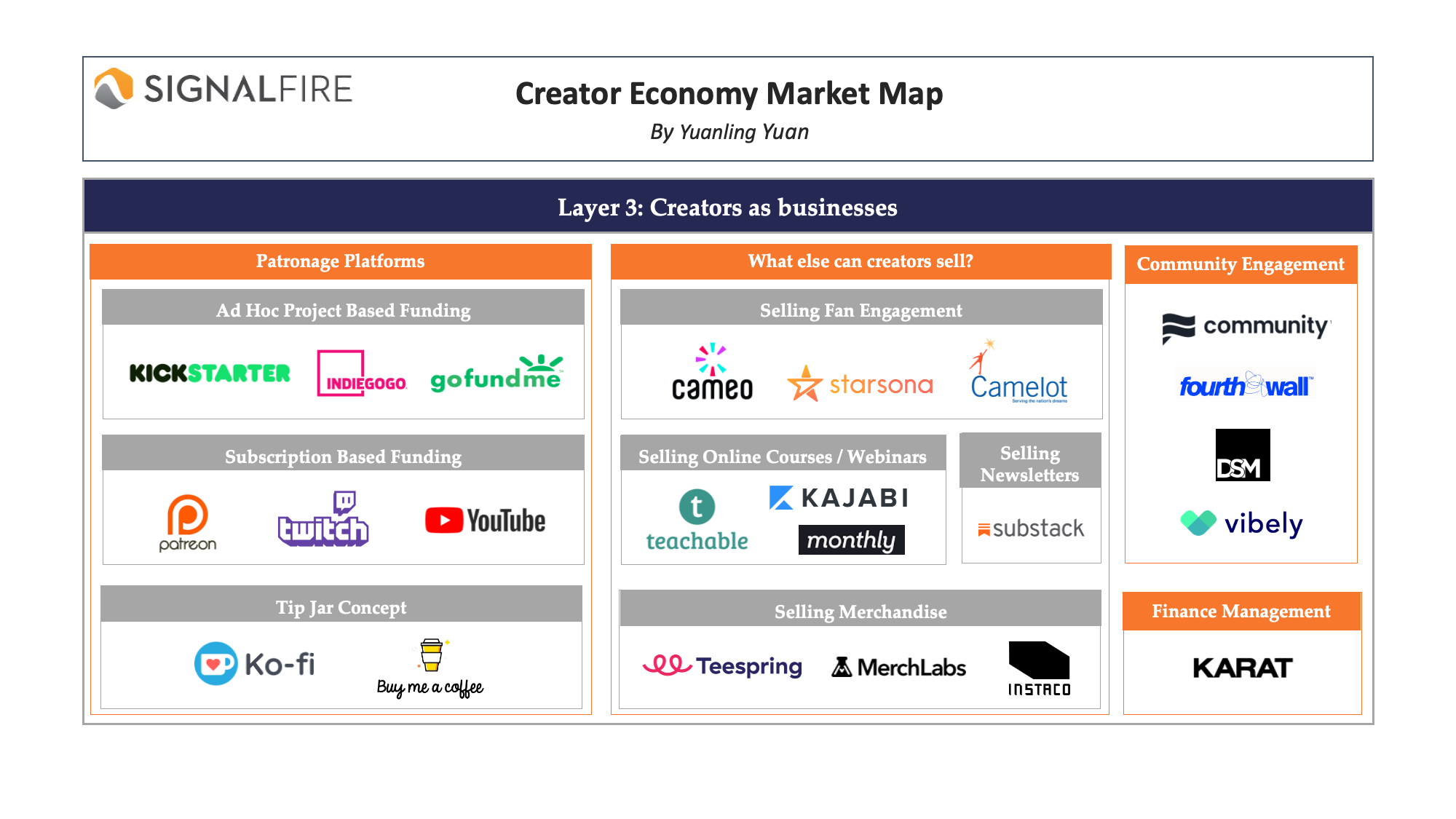

Layer 3: Creators as Businesses

Patronage Platforms

We start by exploring the various donation platforms that allow fans to donate to their favorite creators. There are a few different ways this takes place:

- Ad Hoc Project-Based Funding. We’re all fairly familiar with the big crowdfunding platforms like Kickstarter, Indiegogo, and GoFundMe. Creators use these platforms to publish their one-off books, comics, documentaries, short films, albums, etc. These platforms typically charge a 5% take rate.

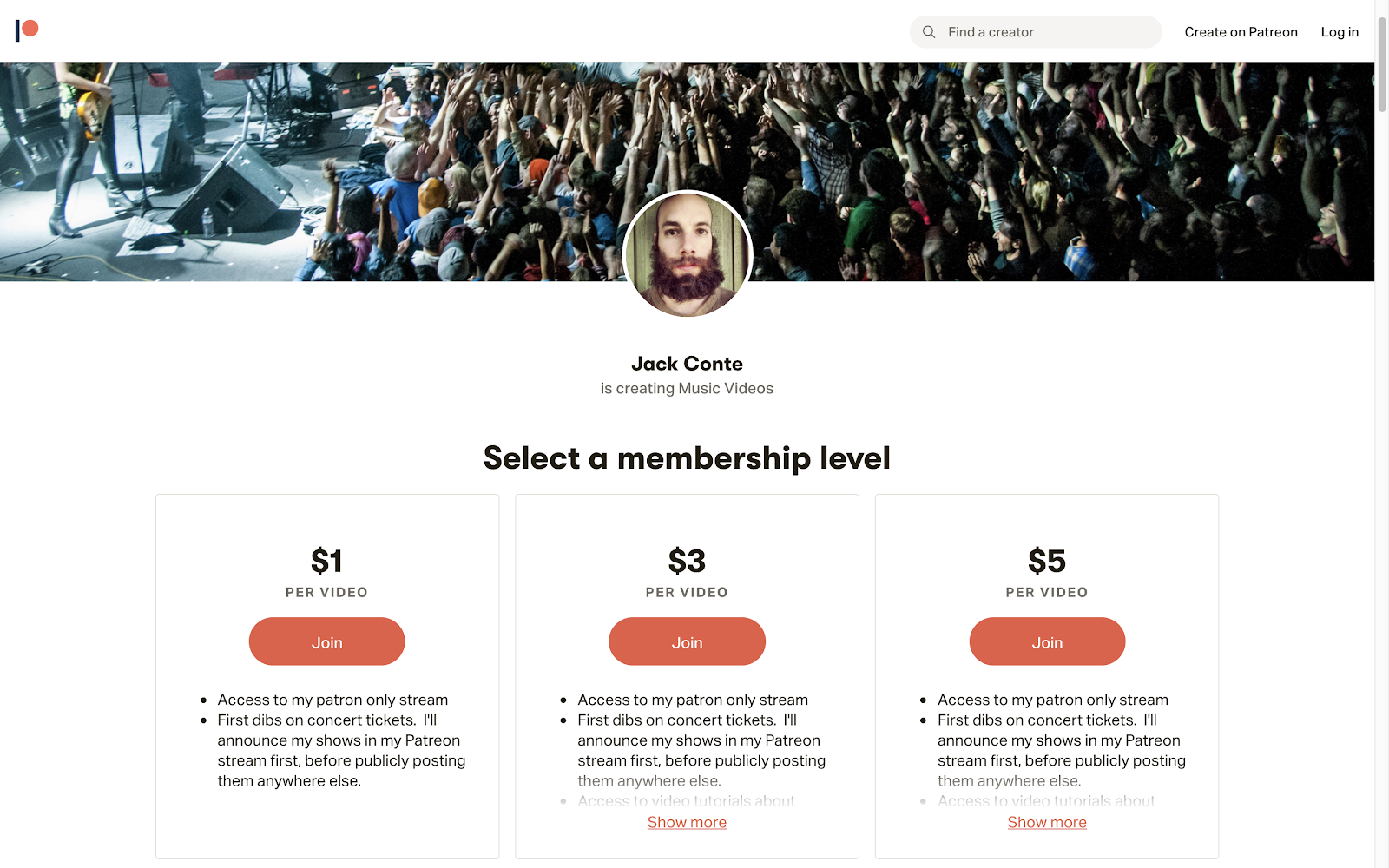

- Subscription-Based Funding. The concept of “subscribing $10/month to your favorite creator” was created by none other than Jack Conte and his startup Patreon, based on the need for consistent financial support for his band Pomplamoose and their music video production studio. More recently, media platforms like Twitch and Youtube Channel Membership have started to build infrastructure for their creators to charge a subscription fee directly on their channels. But some creators can be annoyed if platforms constantly try to cross-promote other content makers to their fans which could increase the first creator’s subscriber churn.

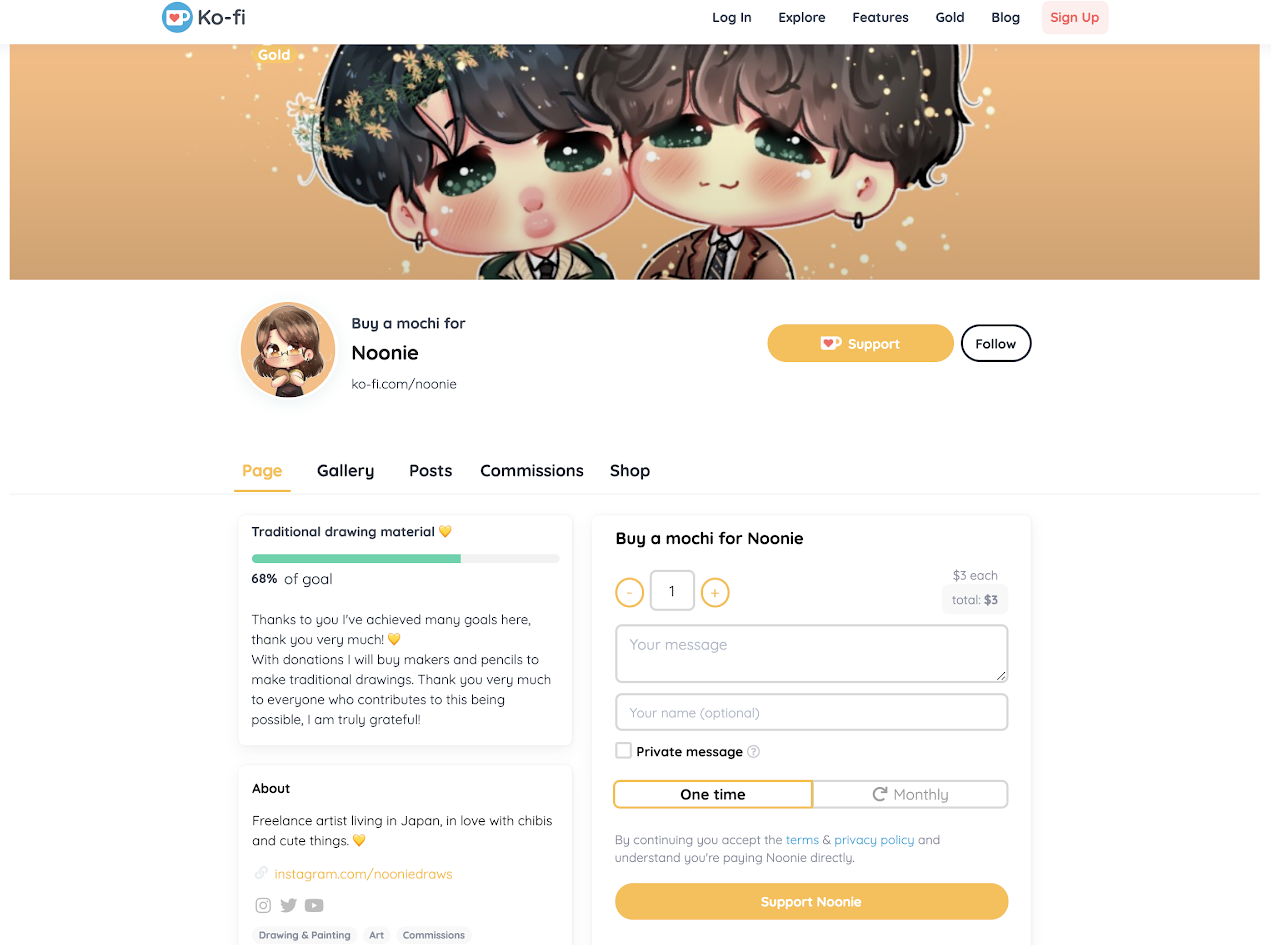

- Tip Jar Concept. Instead of setting up a recurring donation to your favorite creator, you can also make one-time donations, which is much lower friction for fans to get involved. Platforms like Ko-fi and Buy Me a Coffee gives creators the platform to ask fans for $5 here and there. These platforms can let creators reach their maximum audience by not requiring upfront payment, while still offering a way for fans to voluntarily support the creator financially. Some larger social networks also offer ways to tip creators, especially during livestreams, in exchange for shout-outs from their favorite streamers or special badges and added visibility to other fans. This “economy of recognition” can let creators focus on making niche content designed to get their biggest fans to pay, and is advantageous for platforms as they can earn a cut while attracting creators without much work.

COVID Impact? Net neutral. Supply has increased because COVID has encouraged many people to become creators in order to generate additional income streams. For example, Patreon added 30K new creators on their platform in the past 2 months. Patrons who are still financially stable are opening their hearts and wallets with bigger payments for creators. However, this is partially offset by a decrease in demand because as unemployment rises, more people will be cutting discretionary spending on things like a monthly donation to a creator.

Investment Opportunity Assessment

- Pros: Integrated platforms like Twitch or YouTube can charge a high 30-50% take rate because they can leverage the consumer engagement they already have to provide creators a ton of value on building an audience.

- Cons: In contrast, standalone companies have a low take rate of typically 5% because they don’t have additional value add and need to align themselves with the creators. Given that the largest platforms in this space have under 500K creators, a 5% take rate off an average of $10/month donation will be tough to build a large business.

What else can creators sell?

- Selling Fan Engagement. These are platforms that enable creators to sell some type of interaction with a fan. Cameo made flashy headlines in this space by creating a marketplace for fans to pay for personalized video shout-outs from celebrities. Cameo’s success can also be attributed to how easy it was for creators to get paid $50-100 for making a short 30-second video, which rapidly helped them grow their supply side. Starsona takes a slightly different approach by allowing creators to sell all kinds of interactions with fans — 1:1 direct messaging, Q&A, create a playlist for your party, critique a photograph, create a ringtone, etc. Camelot allows YouTube and Twitch audiences to pay for what they want to see (i.e fans can request that streamers “win with no armor”, “add a heartbeat monitor to the stream” or “play a cover of Hey Jude”).

.png)

- Selling Online Courses / Webinars. Platforms like, Kajabi, Teachable, Thinkific, and Podia are online course builders with a full suite of products that enables the creator to market, engage, and monetize their courses. Other companies like Monthly curate their own creator-led courses. Tools like Lu.ma, Airsubs, Stream.club, Via.live, Reach.live, and Mixly let creators sell access to webinars via video chat mediums like Zoom. These are very popular for creators who have a valuable skill to share, such as watercolor painting, cake making, or producing electronic music. These creators often build a large following on one of the social media platforms by sharing tidbits of their skills in ad hoc videos and then redirecting the most engaged learners to their separate online course page.

- Selling Newsletters / ebooks. Substack allows writers to monetize their newsletters. It allows journalists and others to build independent audiences and set a subscription fee for their newsletters. Top writers are able to make $50-100k/year with Substack. All you need is 400 subscribers paying $10/month or 800 subscribers paying $5/month. One such top writer is Luke O’Neil and his popular newsletter Hell World, where he reports the distressing day-to-day American life with a unique stream-of-consciousness style.

- Selling Merchandise. The largest players in this space are Fanjoy and Teespring, which help creators sell apparel and officially integrates with YouTube, Instagram, and Twitch. Others include DFTBA, Represent, and CrowdMade. There are many other companies in this space that do not integrate with the large platforms like MerchLabs and Instaco. While super-fans may buy merchandise from time to time, it is often not a reliable source of income for the creators because it is not something that fans will repeatedly purchase.

COVID Impact? Tailwinds. As the unemployment rate in the US rose, more creators are turning to these platforms to supplement their income.

Investment Opportunity Assessment

- Pros: Companies that can build a robust business model in the entire creator economy should be ones that help creators generate additional income.

- Cons: Will need to examine the business model on a case-by-case basis. For example, selling merchandise has become commoditized and really tough to scale as a business given that it is so operationally intensive.

Community Engagement Tools

Several startups believe that increasing the engagement within the fan community as a first step before targeting them for various sales is crucial to increasing conversion rates. Community helps creators collect fans’ personal phone numbers while DSM is able to message fans across different social media platforms via a single porta, and Zebra lets creators build a dedicated community space for their fans. These platforms aim to create a more direct or efficient mode of communication from the creator to his fans. Vibely allows creators to create regular “challenges” for her fanbase, thereby increasing engagement within the community. Fourthwall on the other hand, creates a dedicated Shopify-like ecommerce page for the creators and enables them to send a personalized video shout-out to fans who’ve made a purchase.

While all these tools have substantial adoption from creators to-date, the way they help creators ultimately monetize a more engaged community is via the selling of merchandise, which as discussed earlier, is not the most reliable source of income.

Finance Management Tools

As creators begin to diversify their income and become more like small-to-medium-sized businesses, they will need more tools to help them manage their finances. Creators also don’t plug well into the existing banking infrastructure because they are very difficult for banks to underwrite — they don’t have W2s and instead have many sources of income that are unpredictable. SignalFire recently invested in Karat, a banking solution for creators. Karat gives creators the ability to aggregate all sources of income onto a single platform, offers income smoothing for creators on a week-to-week basis and provides instant loans based on predictable future income.

Are you building something for creators?

At our early-stage venture capital fund SignalFire, we believe creators and the startups that support them are vital to the future of entertainment, advertising, education, and commerce. That why we’ve invested in startups like Karat’s credit card for influencers and HoloTech Studios’ FaceRig for livestreaming motion capture avatars.

Founding a creator-focused startup? We’d love to hear about it. You can reach out here or to any of our team members. SignalFire brings to the table our Beacon technology for predictive recruiting and market data analysis, our talent team that can ensure you score your dream hires, in-house experts on PR and go-to-market, and our network of 85+ invested-advisors including founders and executives from YouTube, Instagram, Twitter, Adobe, and many more that help support our portfolio companies. Those value-adds are why 85% of our portfolio founders rank us as their most helpful investor. SignalFire can help creator-led startups skill up as entrepreneurs with our programs to assist with fundraising and board construction, while assisting experience founders building creator tools to hire swiftly to seize these new opportunities.

Creators are the new founders

We’re at an inflection point in history where becoming a professionalized creator is one of the most desired jobs. Creators become creators because they love to create. As they grow their audience and expand their revenue channels, the burden of managing the day-to-day of their business grows heavier. Startups that will dominate the next stage of this evolution are ones that are centered around empowering creators to seamlessly monetize while staying focused on what they already love — creating content.

Being a creator today requires evolving from being an artist to being a founder. The job has come to encompass product management, design, community engagement, ecommerce, and data science along with being an entertainer. You have to build a team of experts and vendors to help you manage the tools to build a diversified business across platforms.

But with that diversification comes resilience. Creators become less vulnerable to shifts in priorities of the tech giants or their algorithms by owning the direct relationship with their fans. Each creator can assemble a different balance of revenue streams to match their style, no matter how niche. That’s a big win for everyone, because creators catering to each of our esoteric interests can build a sustainable career. Instead of just homogeneic, lowest-common-denominator primetime sit-coms, we get content tuned to every sub-culture in the rainbow. Now there are finally enough creators to support a whole ecosystem of startups helping them turn their passion into their profession.

Subscribe to SignalFire’s newsletter for guides to startup trends, fundraising, and recruiting

Yuanling Yuan

Partner

Yuanling (she goes by "YY") is a Partner at SignalFire and focuses on venture and growth stage investments in healthtech, legaltech, and other vertical AI. Prior to SignalFire, YY worked on the investment team at Blackstone's Strategic Opportunity Fund.