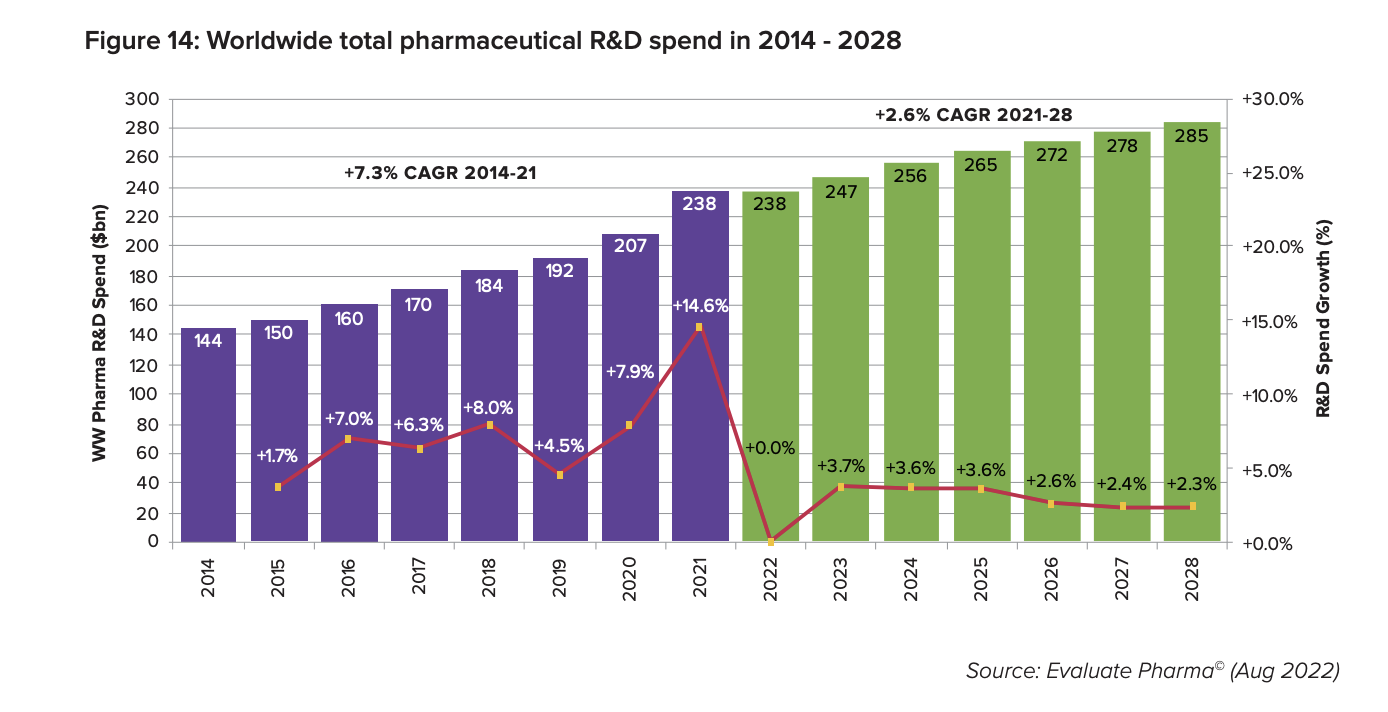

The race to launch new medicines is moving faster than ever, accelerated by increased competition, new data sources, and a coming wave of software tools. Biopharma companies now spend $247 billion per year on clinical R&D, plus $30 billion on marketing drugs to patients and physicians. It’s no wonder startups are clamoring to sell into the industry despite stiff challenges with go-to-market, compliance, and integration.

Biotech venture investment has declined, IPO activity has slowed, and the XBI (an index of U.S. biotech stocks) was down almost 50% from its peak in early February 2021 through mid-February 2022. Despite the biotech winter, there are green shoots that indicate summer is coming.

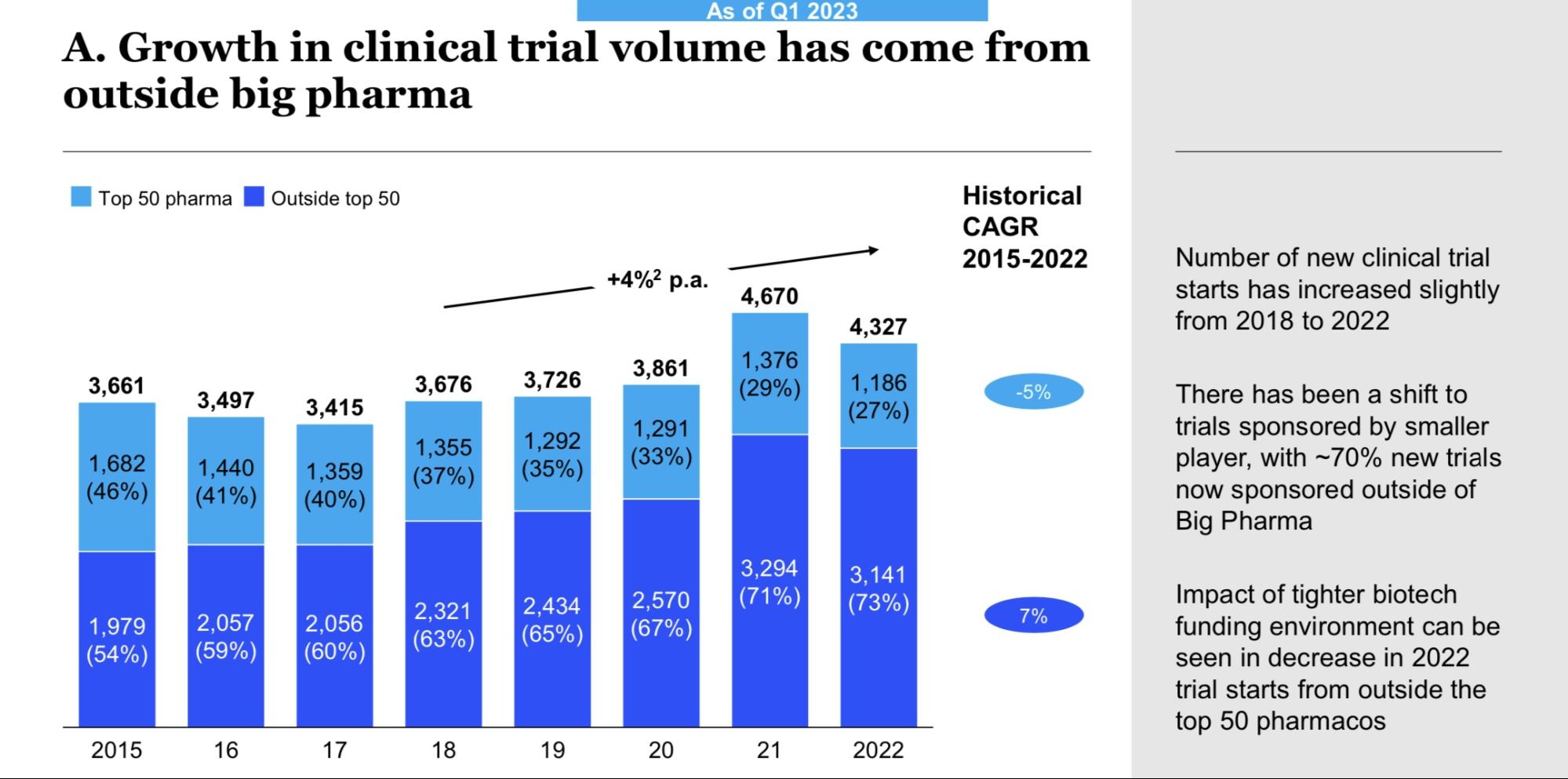

The XBI has rallied 27% since its 52-week low in October, and clinical trial activity remains robust. In 2022, 4,327 trials were conducted—a drop from 2021 but still a 12% increase from 2020. The need for software solutions to expedite drug development remains higher than ever and may prove to be a recession-resistant area of the market. As one clinical research organization expert I spoke with remarked, “There will always be money for good science.”

Which solutions inspire such demand that their builders can overcome the hurdles of selling into pharma? And what should founders know about the esoteric buying patterns of the pharma world? I spoke to dozens of pharma giants, experts, and founders in the space to get their input. Here’s the roadmap for where the biggest venture opportunities are and how those companies can grow the fastest, starting with a few takeaways.

Highlights:

- The proliferation of data around drug discovery is creating demand for modern software infrastructure.

- Outdated data capture and patient engagement practices are reducing the effectiveness of clinical trials, delaying the rollout of new medications.

- The adoption of newly commercialized medicines could be vastly accelerated by tools to educate both physicians and patients.

- Truly differentiated data sets on valuable patient demographics are rare but extremely useful in a sector where most players draw from the same data sources.

- Since pharma giants lack integration teams and data scientists, software subscription startups may need to build small, efficient services teams to get customers up and running.

Startup opportunities in the modern pharma/biotech stack

The new pharma technology stack encompasses core infrastructure, enhanced research capabilities, and systems of record, transforming the way novel medicines are discovered, developed, and distributed. It has become increasingly inefficient for biotech/pharma companies to build internal tools that can compete with these specialized offerings. While purpose-built software for pharma’s needs is not necessarily new, there’s an opportunity to replace clunky, legacy solutions that have not been updated for 10–15 years.

“Everyone has rethought their operating models. The focus is on better, faster, and cheaper drugs for patients. Pre-COVID, people would laugh at me if I said a drug could go from preclinical to commercial in 24 months. But now it has happened, so we’re trying to find new use therapies.”

—Executive at a leading CRO

Here’s a closer look at the tech needed, from R&D to commercialization.

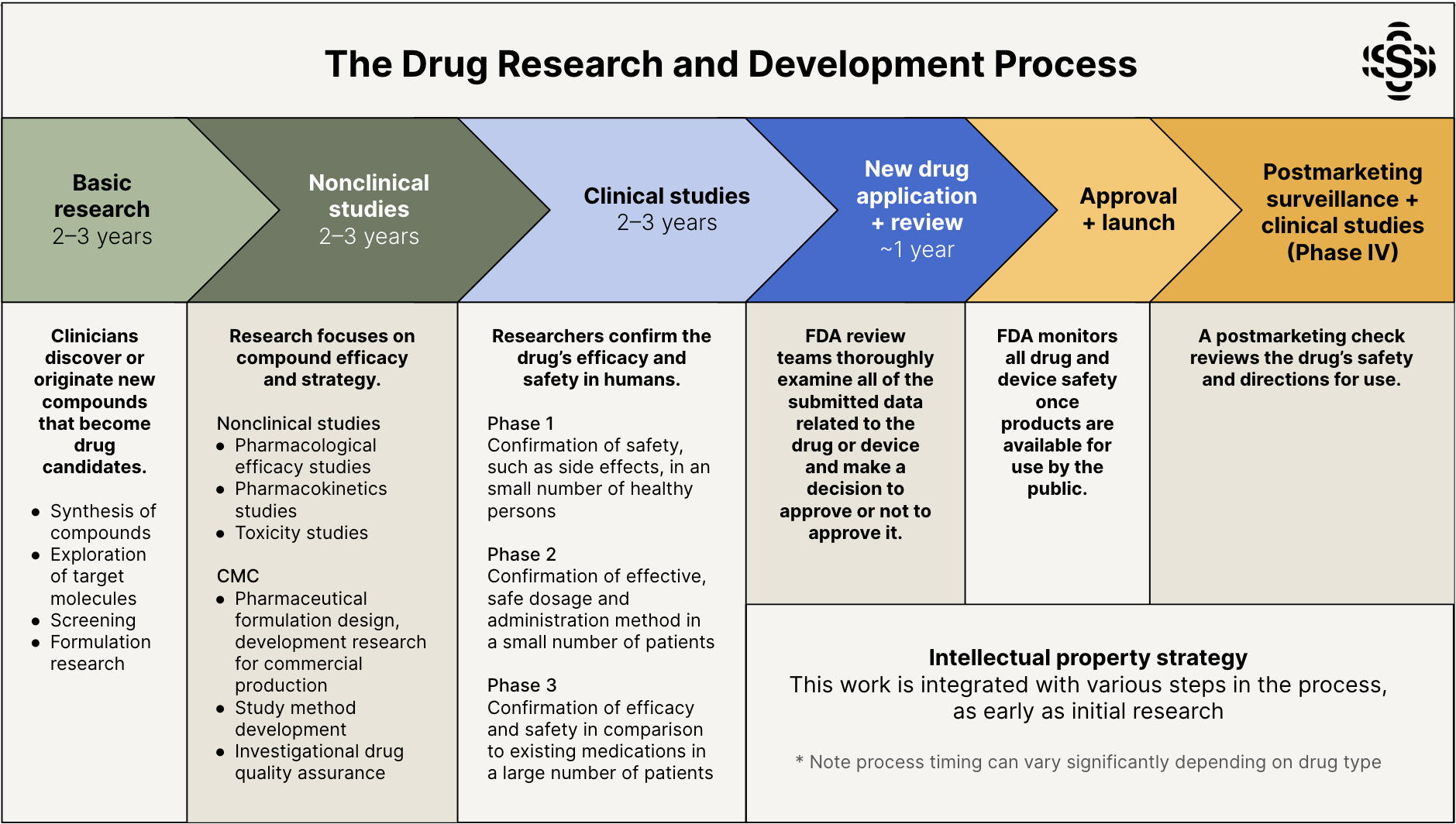

Drug research

The discovery process in biotech involves continuous cycles of experimentation, analysis, and iteration. With increasingly sophisticated lab instruments and complex multiomic data, there is a need for modern infrastructure to handle the massive amount of unstructured imaging data. Unique data sources and software tools designed by science-fluent founders in real-world evidence (Komodo) and natural history studies (Ciitizen) are revolutionizing the way research is conducted and insights are generated. Data services businesses, managed and enhanced by their creators, can offer network effects and incremental value as more users join and more data is ingested.

Clinical studies

Clinical trial infrastructure needs a tech overhaul. Outdated processes, such as paper-based data capture and inefficient trial management, contribute to low enrollment rates, high dropout rates, and delays. Tools for electronic data capture, trial management (Veeva Vault), patient recruitment (Reify Health), clinical trial acceleration (Unlearn AI), and decentralized trials (Medable) can enhance efficiency. Given the complexity of clinical trials, there are $1B+ market opportunities in the office of the CFO such as dedicated FP&A (Auxilius), clinical trial payments (Greenphire), and gross-to-net (Integrichain) once a drug goes commercial. Selling into contract research organizations (CROs, like IQVIA) that typically manage much of the clinical trial process for large pharma is common, compared to selling directly into the pharma companies themselves.

Launch and postmarketing

The goal of any medicine is to reach the patients who need it. However, barriers such as middlemen, pricing opacity, and complex supply chains hinder the distribution process. Software tools can offer solutions for customer relationship management, targeted physician engagement, patient education, and financial assistance. Modern infrastructure ensures compliance, quality control, and regulatory requirements are met, optimizing the commercialization and distribution of drugs.

Essential traits of successful early-stage pharma tech startups

Selling into pharma isn’t like building for the traditional enterprise world. Pharma giants don’t have enormous software integration teams ready to connect startups’ tech into their systems, nor data scientists waiting to analyze raw outputs. Experience around sales for the industry is a superpower, and being able to customize solutions to win a giant contract can make the difference between booming revenue and shutting down. Building the following characteristics into pharma tech startups gives them the best chance for success and fundraising:

Entry point into large pharma

The top 25 largest pharma companies account for the majority of all pharma sales. They have the biggest budgets in healthcare as well as significant fragmentation within an organization for licensing data. To provide a sense of how massive these budgets are, there are dozens of people at Pfizer who can sign six-figure contracts without requiring major approval. Most companies need to win large pharma contracts and also capture some of the longtail of smaller biotech to become $1B+ businesses. Whether through a savvy sales strategy, a founder or sales exec’s rolodex, or a product solving a burning need, startups need a way to lock in their first flagship customer.

Selling to big pharma for the first time without significant services is not easy, but it gets a lot easier once you’re in. Be prepared to come up against competition from internal teams and long sales cycles. The way that some of the most successful pharma/biotech software companies (e.g. Benchling) have penetrated large pharma in the past has been somewhat serendipitous through industry consolidation.

As the most promising biotechs get snatched up by larger pharma, there are a few scenarios for the fate of existing software tools: (1) axed by the acquirer, (2) retained by the acquirer (common if crucial to a particular clinical trial), or (3) upsold into a much larger contract if the pharma company sees value for use in its broader portfolio. Similar to other vertical software companies, there’s a unique opportunity to capitalize on the “virality” of being focused on a particular industry. Individuals within biopharma often move to other companies within the industry and take their favorite tools with them.

People have long believed that startups must sell into large pharma in order to reach any real scale. Large pharma remains the highest ACV / lowest churn potential customer, but midsized biotech companies have been steadily growing in recent years. Emerging biopharma companies now make up the majority of the spend on CROs today and are responsible for two-thirds of the molecules in the R&D pipeline, up from 51% in 2017 and one-third in 2002. (Emerging biopharma companies are defined as those with <$200M R&D spend and <$500 in annual sales.)

Deep proprietary data sets and/or advanced analytic capabilities to make meaning of data

The need for up-to-date and accurate data across all aspects of the value chain is higher than ever due to increasing competition and accelerated timelines. Patents have a limited shelf life, so it’s paramount to maximize value from every commercialized product over the patent length in order to generate a return on very high R&D investments.

Data sources are often not a major differentiator as most platforms buy from similar data providers, especially in the case of real-world evidence (RWE) platforms. RWE plays can often peter out because of the commoditized and crowded category, making it hard to create venture-backable outcomes. While almost all data networks have very similar breadth due to the same upstream tributaries, the layering and contextualization on top of this basic data can help differentiate them—many pharma companies do not have the data scientist resources to quickly analyze raw data. Truly unique and complete patient data (especially in hard-to-find areas like rare diseases) is invaluable, and pharma companies will pay for this data for research, sourcing clinical trial participants, and commercial use cases.

The adoption of AI will change how this data is consumed—more to come from SignalFire on how early-stage startups can partner with corporates to get access to training data.

Scalable business model with limited services relative to software subscription revenue

Pharma companies aren’t going to pay significant dollars to do their own implementation, so it can be hard to sell software to large pharma without some services involved. Traditional CROs like IQVIA are service businesses, but newer startups in the space have automated much of the inefficient human involvement in getting customers the information they need. Still, minimum viable services can be necessary in the beginning (and tend to be what pharma companies are most comfortable with vs. paying for subscription software).

Why SignalFire: A firm steeped in the next generation of pharma tech

Given the nuanced nature of developing and selling products for pharma, experienced advisors and robust value-adds around go-to-market can give startups a leg up. SignalFire is well positioned to support companies in this vertical given our deep expertise in the sector, data software tools, and network of industry and in-house mentors. With PhDs in ML and data science, we can help companies deepen their technical moat. We developed our Beacon AI data platform to provide portfolio companies with an elite talent search engine to build their best team. And we have industry advisors around the table with decades of experience in pharma who can help navigate the complexity of selling to these large institutions.

If you’re building a software startup in the biopharma space, we’d love to help you accelerate the future of drug development!

Sooah Cho

Partner

Sooah is a Partner leading the early-stage investment practice in Health and PharmaTech. Prior to SignalFire, she was a product leader at CVS Health and Devoted Health, and led fast-growing B2B software investments at Underscore VC. As a product builder, GTM strategist, and policy nerd turned investor, she partners with founders at the earliest stages of their discovery, building, and scaling journey.